Looking Beyond Assets Under Management: European Managers To Focus More On Revenue Growth

AUM IS NO LONGER A PROXY FOR BRAND STRENGTH Assets under management (AUM) has historically captured the headlines in the fund management business. It has generally been a proxy for a fund manager’s brand and financial strength. And while it retains its use as a proxy for brand strength, it is losing its value as […]

AUM IS NO LONGER A PROXY FOR BRAND STRENGTH

Assets under management (AUM) has historically captured the headlines in the fund management business. It has generally been a proxy for a fund manager’s brand and financial strength. And while it retains its use as a proxy for brand strength, it is losing its value as a measure of financial success. With the business still centred on asset-based fees, the growth of low-cost indexed solutions in developed fund markets has meant that asset growth generates less new revenue than in years past. Revenue growth is increasingly lagging asset growth as a result, breaking the historical tango between the two measures.

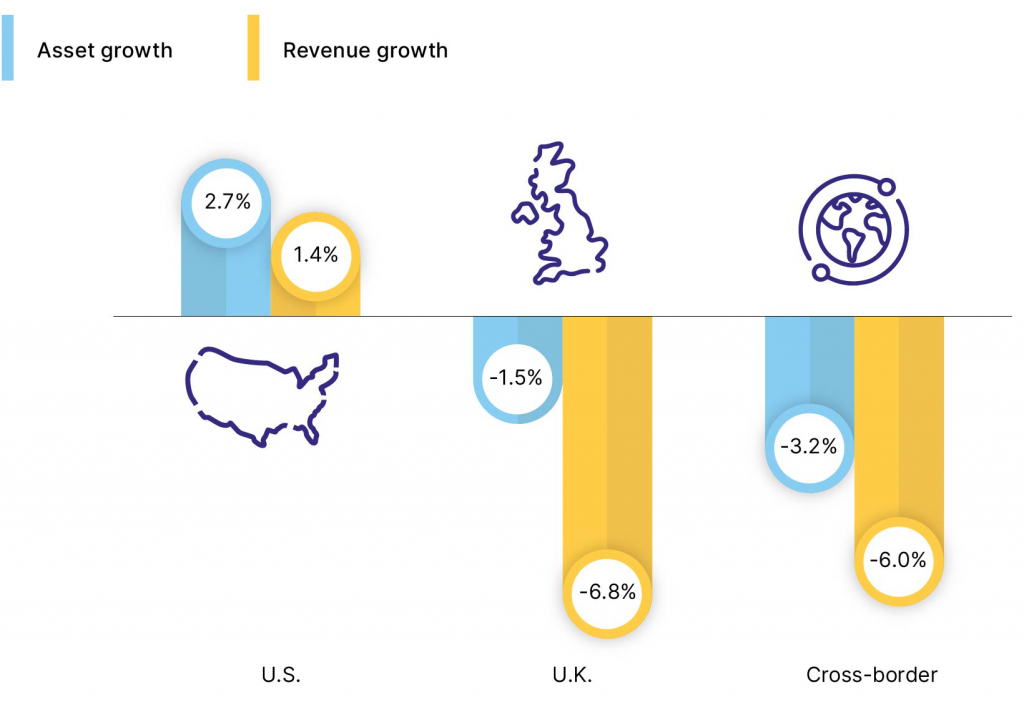

Highlighting this is a recent white paper from ISS Market Intelligence, Growing Revenues, Not Assets, New Name of Game. The white paper shows this dynamic playing out across markets, with the gap between asset and revenue growth widest in the UK and the European cross-border markets of Ireland and Luxembourg (see Figure 1). For the UK and the cross-border markets, the growth gap was 5.3% and 2.8%, respectively, compared to a 1.3% gap in the United States.

Figure 1: Across Markets, Revenue Growth Weak

Estimated growth in long-term fund revenues and average assets under management, 2023

Source: ISS Market Intelligence.

Note: Data exclude money market and fund of funds. Cross-border includes Ireland and Luxembourg-domiciled funds.

PASSIVE AGGRESSIVE(LY) WINNING

Passively-managed index funds have made great strides across both sides of the Atlantic and have upended the fund business in myriad ways. In fact, the United States grabbed the headlines recently as index solutions recently crossed the 50% mark in terms of long-term investment fund AUM. Such solutions, meanwhile, accounted for about 30% of AUM at the end of 2023 in Europe, including the United Kingdom. Although behind the United States in terms of adoption, these two markets have witnessed index funds’ long-term AUM share increase by more than 15% in the past decade.

While no single factor has contributed to the rise of index solutions on both sides of the Atlantic, the shift amongst advisers from commission-based to fee-based pricing structures has been a key contributor. The separation of advice fees from product fees created fertile ground for advisers to request fee reductions, either in the form of lower cost funds or share classes, from their asset management partners. Lower investment fees have served as a means for advisers to control the overall cost-to-customer of investing without having to sacrifice their advice fees.

Fee-based adoption by advisers can occur both naturally and via regulatory action. In the UK, it was regulatory action that truly moved the dial amongst retail advisers. The Financial Conduct Authority (FCA), banned embedded commission as part of its Retail Distribution Review (RDR) in 2012, thus driving the adoption of fee-based pricing. Since that time, index solutions have witnessed their share of long-term AUM increase by 19%, and the FCA has since introduced further legislation that puts the onus on the investment community to justify fund costs. This includes the FCA’s Assessment of Value rules, whereby funds must justify their costs, and Consumer Duty, which in simple terms requires all financial transactions to undergo a client cost/benefit analysis.

ESG: AN ACTIVE SAVIOUR?

Whereas index adoption can be observed taking hold in a steady manner in the UK, the European Union (EU) marketplace has seen the fortunes of active management vary considerable over the past five years. Following the implementation of the EU’s Sustainable Finance Disclosure Regulation (SFDR), a surge in investment fund flows poured into environmental, social and governance (ESG)/sustainable managed active funds. Sales of active funds covered by Articles 8 and 9 of SFDR spiked in 2020 and 2021, garnering over €500 billion in net sales. This surge, however, reversed to an outpour in 2022 and 2023, with net outflows of these funds totaling €250 billion. Sustainable investing, nonetheless, remains largely an actively-managed affair in the EU, with index solutions accounting for just 15% of the fund AUM covered by Articles 8 and 9. This compares to 44% for Article 6 funds, which are not primarily sustainably focused. If fund buyers continue to equate sustainable solutions with active management and these solutions return to fashion, index funds may witness significantly less index fund adoption in than in the United States.

RISE OF THE ETF

The growth of indexing is also a product innovation story. On both sides of the Atlantic, exchange-traded funds (ETFs) have grown by leaps and bounds in the past decade. In Europe, long-term ETFs have crossed the €1.5 trillion asset threshold in 2024—and show no signs of slowing down. Flows remained positive throughout the challenging years of 2022 and 2023 amid significant barriers to further retail adoption of ETFs; ETFs are not widely available or efficiently transactable across many adviser and do-it-yourself platforms in Europe (including the UK). ETFs in Europe gained traction early on with institutional investors and high net worth investors given their propositions around cost and liquidity. Interest, however, is building beyond the original investor base.

SHAKE IT OFF

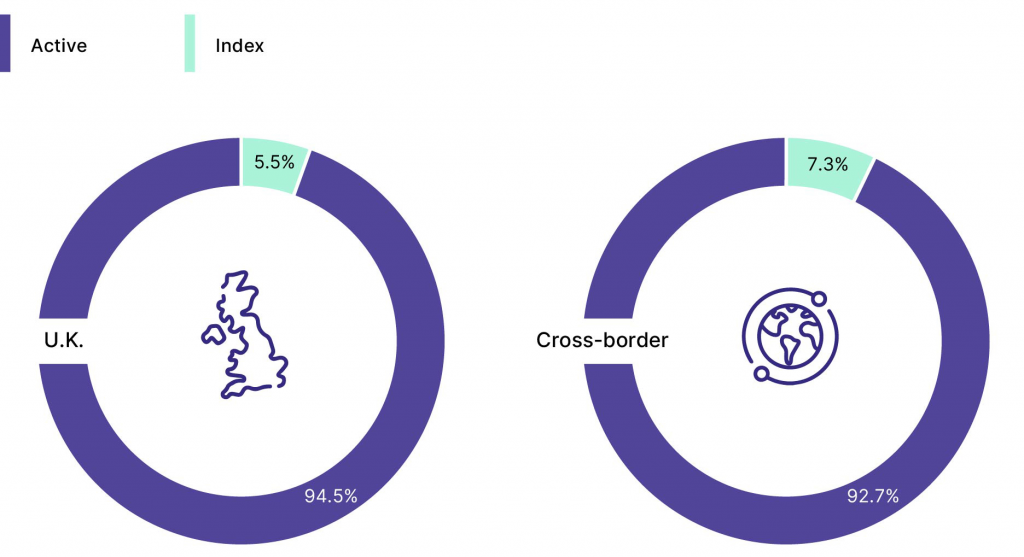

All is not lost for active management, however. Indeed, active management still generates the lion’s share of the revenue stemming from investment funds in the analysed markets. Even with index solutions representing 30% of long-term AUM, actively-managed funds account for well over 90% of the revenue pie in the UK (see Figure 2), Ireland and Luxembourg. The opportunity to win in the active space—even if it is a shrinking opportunity—remains an attractive one. Building a commiserate revenue base from passive funds, which can be priced at a fraction of their active counterparts for core mandates, would prove a near-impossible task for today’s active managers. Even in the United States, where active managers have suffered a steeper fall in AUM, revenues still account for more than 85% of AUM. And while asset managers in the United States saw profitability sink in the 2010s, coinciding with a period of strong passive fund growth, asset managers have seen restored operating margins—at least for a while—in the opening years of the 2020s.

Figure 2: Index Funds Gobbling Market Share in Europe, but Active Funds Still Revenue Giants

2023 estimated share of revenues, long-term UK and cross-border funds

Source: ISS Market Intelligence.

Note: Data exclude money market and fund of funds. Cross-border includes Ireland and Luxembourg-domiciled funds.

LOOK WEST, YOUNG MANAGER

Today, Europe’s position in terms of index solutions’ share of revenue and AUM parallels that of the United States a decade ago. European managers—both active and passive—may therefore wish to look west to determine their best course of action. Consolidation was at the heart of many U.S. active managers’ response to increased index adoption. Since 2014, one-third of U.S.-domiciled active funds in existence at that time have been closed. Most recently, U.S. managers made notable efforts to clear cluttered product shelfs, opening up shelf space and resources to turn their efforts to innovation. While active fund launches outpaced ETF launches, which were predominately index-based up until 2020, active managers have begun to pivot. Responding to the growth in the U.S. ETF market, around 200 active managers have launched active ETFs.

European fund shelves appear ripe for consolidation. The UK, Ireland and Luxembourg have over 15,000 domiciled funds, and manager consolidation also appears to be a possibility, with more than 500 managers operating in those jurisdictions. What is less certain is where attention is turned beyond traditional fund structures. While active ETFs are growing in Europe, they remain miniscule, and active ETF adoption lacks a clear path amongst retail clients across Europe, as there was in the United States, as platform and distribution dynamics have created barriers. Nonetheless, active fund managers are likely to find new narratives if they hope to combat the market share losses seen in the United States in the coming decade. Expect ETFs, sustainability and the alternatives to be part of that story.

A NEW ERA OF GROWTH

In Europe, much of the landscape remains uncertain. That fund managers will need to focus more on the revenue generating and profitability, however, does not. Index investing has changed the game. Barring strong market growth, industry revenues appear ready to stagnate. Increasingly, fund managers may also find themselves with less pricing power as consolidated buyers in institutional or retail channels rise to the forefront. In response, expect fund managers to be selective in expanding to new markets and more ruthlessly rightsize operations where growth prospects dim. To borrow terminology from the portfolio community, the decade ahead will be defined by growth at a reasonable price (GARP). When evaluating new opportunities, fund managers will seek to strike a fine balance between the earning potential of an opportunity—a function of both investor willingness to pay and available assets—against the costs of entering that market: AUM alone, will no longer suffice.

The full global white paper Growing Revenues, Not Assets, New Name of the Game is available via MarketSage from ISS Market Intelligence.

By: Benjamin Reed-Hurwitz, Christopher Davis